Logistic regression is used for binary classification.

It is quite similar to a simple linear regression in the sense that the objective is to find optimal weights $\omega$ to predict a variable. However, in the logistic regression we use a sigmoïd function.

Rem: “logistic” because the logistic law has a sigmoïd function as a repartition function.

Rationale behind the use of the sigmoïd function:

We look for the à posteriori probability $\mathbb{P}(x | y=1) = \pi (x) = \hat{y}$.

The predicted variable $\hat{y}$ is thus a probability.

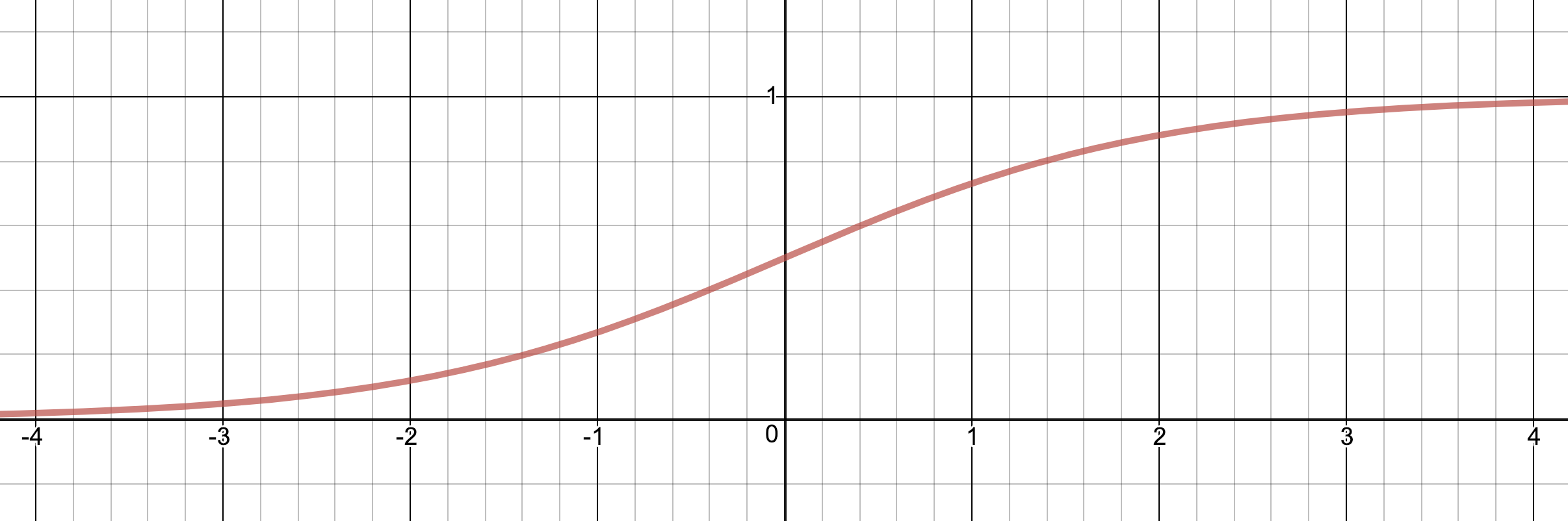

The sigmoïd function: $\sigma: z \to \frac{1}{1+e^{-z}}$ is well adapted because we want an output that is included in $[0,1]$.

Why is sigmoid often preferred to classical normalization? E.g. a classical normalization of $[a,b]$ would be $a’ = \frac{a}{a+b}$ and $b’ = \frac{b}{a+b}$. Let’s consider a neural network. A network should typically output larger numbers when the prediction is better (source); we thus want a normalization that can take this behaviour into account. However, the classical normalization would give same results, not matter the scale. E.g. $classical\_normalization([0.5,0.9]) = classical\_normalization([5,9])$. On the contrary, the transformation through sigmoid gives a clearer picture when the numbers are bigger. E.g. $sigmoid\_normalization([0.5,0.9]) = [0.29,0.71]$ but $sigmoid\_normalization([5,9]) = [0.01,0.99]$

Classification function: $\widehat{f}_{\omega}(x) = \sigma(\omega x)$ with a threshold.

Loss function

If $y = 1$, we want $\sigma(\omega x)$ to be high => $1 - \sigma(\omega x)$ should be low. The loss function should be increasing with $1 - \sigma(\omega x) = 1 - \frac{1}{1+e^{-\omega x}} = \frac{1}{1+e^{\omega x}}$. Equivalently, it should be increasing with $1 + e^{-\omega x}$.

More generally, the loss function is defined as such: $\ell(f_{\omega}, (x,y)) = log(1 + e^{-y \omega x})$ (adding $y$ in the expression allows to take into account cases when $y = 1$ and $y = -1$).

Recall that the log is a monotonic function.

Estimation

The advantage of the logistic loss function is that it is a convex function. Hence the ERM problem can be solved efficiently using standard methods.

Estimation is done using maximum likelihood. Maximum likelihood is finding the parameter that maximizes the probability to have a specific event $(x_i, y_i)$. We want to maximize the à posteriori probability that depends on $x$:

$L(\omega, b) = \prod_{i=1}^n \pi(x_i)^{y_i}(1-\pi(x_i))^{1-y_i}$

This equation has no analytic solution. We use a numeric method to find the optimal parameters (see optimizaton algorithms).

See Neural Network section for more details on optimization.

Note: logistic regression is really a linear model since the objective is to find $\omega$ that is the slope of the line $\omega ^Tx + b$.